Oil, the Dollar and Geopolitical Developments

Market Insights Newsletter

Prepared by the ACG Team

Introduction

Oil is a commodity that, when observed together with the US dollar and inflation expectations, tells a lot about what the market is pricing and what future implications this may bring.

Today we are looking at how this relationship is evolving, given current geopolitical tensions currently in place. The main topics covered are:

- The US dollar as a potential indirect hedge during geopolitical turmoil.

- Oil pricing often involves USD appreciation in stressed scenarios.

- Commodities have been soaring, while breakeven inflation has remained mostly in neutral territory. Higher rates usually come along with a stronger US dollar.

- As of today, the US is the most dovishly priced G10 economy via Overnight Index Swaps.

Oil, the Dollar and Geopolitical Tensions

As of now, the US dollar continues to stand out as the primary winner from the turmoil in the Middle East. Its strength is underpinned both by its traditional role as a safe-haven asset and by the United States’ status as a net exporter of energy, in contrast to most other major currencies, which belong to economies that rely on energy imports.

Historical patterns linking the dollar to oil supply disruptions indicate that the currency may still have room to appreciate further.

At first glance, the overall correlation between the dollar and oil prices appears only modestly positive, largely because oil prices frequently climb during phases of robust global expansion. During such periods, investor risk appetite is strong, and the dollar tends to lag behind more growth-sensitive currencies like the pound and the euro.

Consequently, oil rallies driven by stronger growth tend to soften the more pronounced positive relationship that typically appears during supply-related shocks.

Historical Reference: Ukraine Energy Shock

To understand how the dollar should respond to the current energy shock, it is therefore more instructive to examine a similar episode triggered by supply constraints.

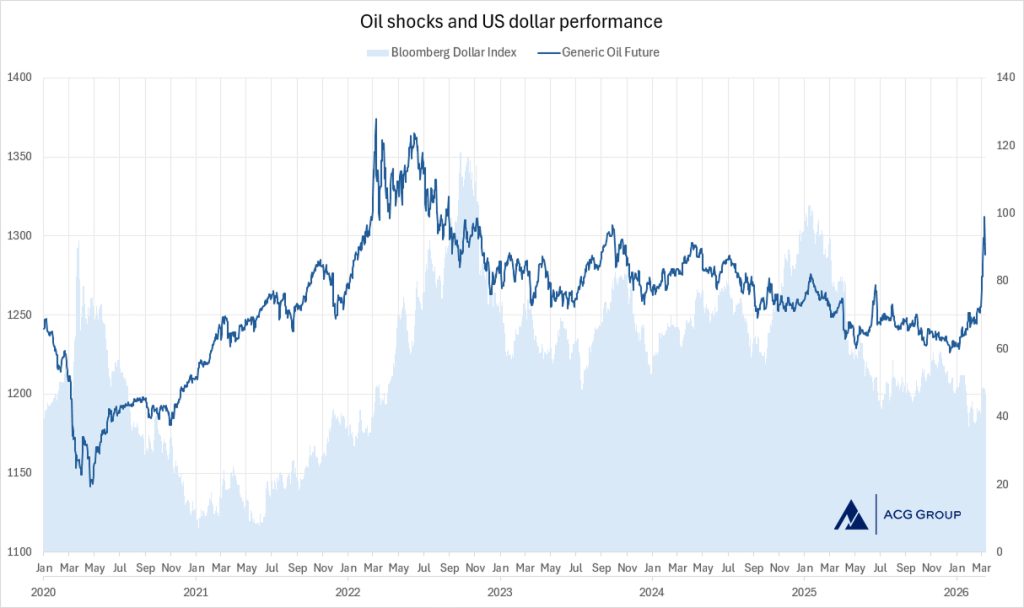

One useful benchmark is the Russian invasion of Ukraine, when energy dynamics dominated financial markets. In that instance, Brent crude surged by about 32% from the onset of the invasion to its high point roughly three months later.

The BBDXY initially trailed as investors evaluated the broader economic consequences, but it eventually reached its peak a few months afterward, climbing more than 15% from the invasion date.

Chart 1. Oil shocks and US dollar performance

Source: Bloomberg, ACG Team analysis.

Using that same relationship to interpret the present situation, with Brent having climbed more than 20% over the past two weeks amid escalating worries about Iran, this would point to potential dollar appreciation of nearly 9%, compared with the roughly 2% increase recorded so far, were the same pattern to reiterate.

It is also important to remember that when the invasion of Ukraine began, the dollar had already risen about 6% from its pandemic-era trough. In contrast, it is now recovering from heavily bearish positioning and negative sentiment, after recently falling to its lowest level in four years.

Monetary Policy Context

Inflation Expectations and Commodities

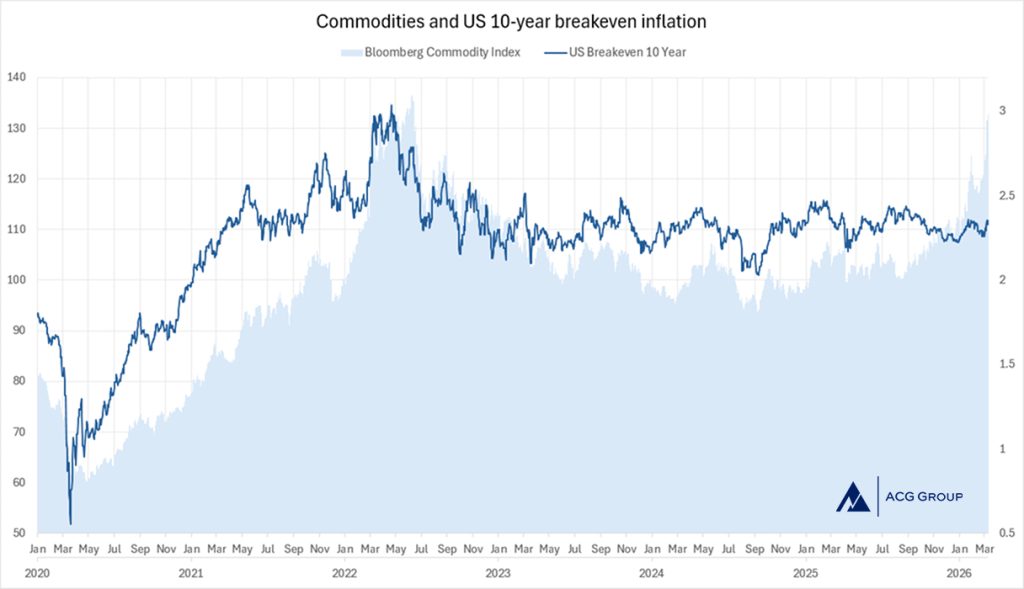

Another interesting aspect to point out is that commodities have been surging in the past months while breakeven inflation has remained relatively stable (10-year breakeven in the picture).

The potential inflation push deriving from this could be a reason for the longer end of the curve to grind higher, potentially triggering a dollar revaluation.

It remains to be seen how long this dynamic might persist.

Chart 2. Commodities and US 10-year breakeven inflation

Source: Bloomberg, ACG Team analysis

Conclusion

Taken together, the above-mentioned points suggest that the dollar may still have room to appreciate, but this will, of course, depend on how persistent cross-border tensions prove to be.

Geopolitical turmoil often comes with safe-haven assets providing a strong cushion to portfolios, but it also depends on how such assets fit among other portfolio constituents.

Now more than ever, cross-asset correlations play a key role in determining whether investment ideas prove to be useful or simply a duplication of already deployed strategies. This is where the real added value comes into play.

Disclaimer

This newsletter is provided for informational and marketing purposes only and does not constitute investment advice, investment research, or an offer or solicitation to engage in any investment activity.

Past performance is not indicative of future results.

See full legal disclaimer.

For a more detailed discussion on how investors may position portfolios in light of the dynamics described above, please feel free to contact the ACG Team at: acg.group@acg.group

Prepared by

ACG Team