Inflation Dynamics and Asset Allocation in a Shifting Regime

Market Insights Newsletter

Prepared by the ACG Team

21.04.2026 | Industry Insights

Introduction

As a follow-up to our previous newsletter on how geopolitical tensions affect market prices, today’s focus is on inflation and how asset classes behave during such destabilising periods.

Key topics:

- Nominal rates and current inflation catalysts vs past scenarios.

- Asset class behaviour in an inflation regime.

- Asset allocation in a regime shift: conclusion.

Nominal rates and current inflation catalysts vs past scenarios

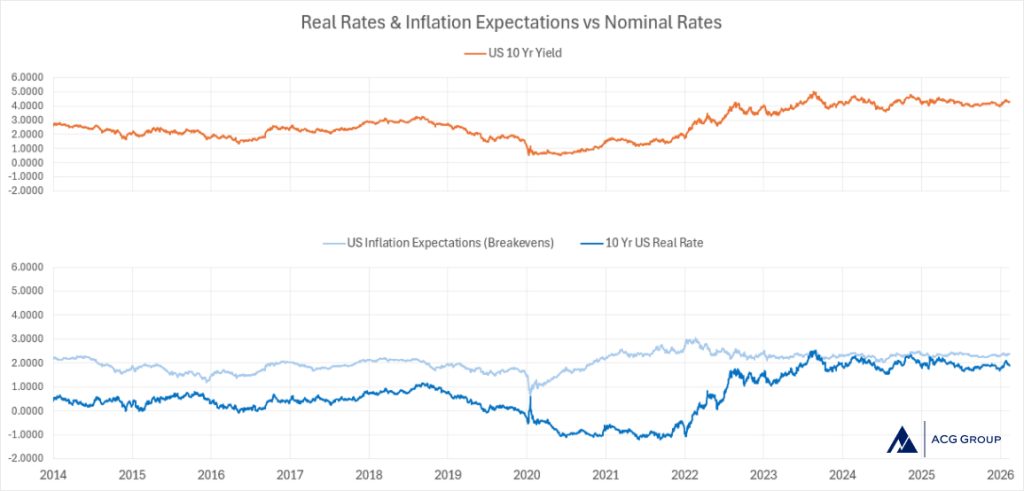

Looking at published consensus, the risk of rates moving materially higher today is generally smaller than in 2022, as the underlying drivers have changed.

Back then, the shock from the Ukraine war and the post-pandemic reopening triggered a sharp rise in inflation expectations, pushing both nominal and real yields higher simultaneously. Markets were repricing a new inflation regime, and central banks were seen as being behind the curve, forcing an aggressive adjustment in rates.

Today, inflation expectations are already partially embedded at relatively elevated levels in nominal yields through breakevens. Many investors believe that much of the inflation risk is already priced in, raising the bar for further increases in rates.

Unlike in 2022, a move higher in yields would now require a new and sustained inflation shock rather than a continuation of existing trends. At the same time, real rates are already at restrictive levels, limiting how much further they can rise without excessively tightening financial conditions.

Investment professionals broadly expect central banks to be at or near terminal rates, with rates more likely to trade within a range, where carry and positioning play a bigger role than directional moves.

The key question remains: should we rely on current market optimism, or should ongoing geopolitical tensions reshape how investors approach asset allocation?

Chart 1. Real Rates & Inflation Expectations vs Nominal Rates

Source: Bloomberg, ACG Team analysis.

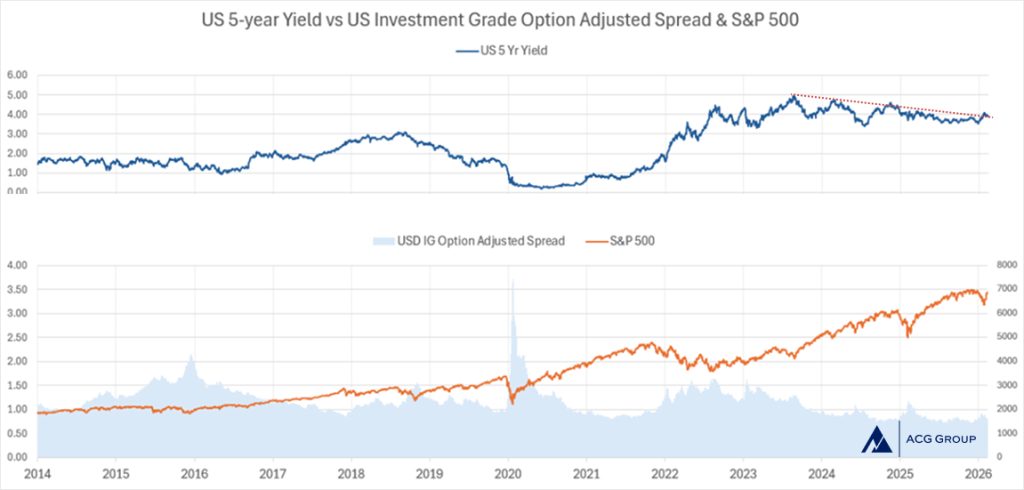

With regards to DM credit, the contrast with 2022 is also clear.

Back then, spreads widened sharply due to the combination of rising rates and recession fears. Today, higher base yields provide a cushion, allowing credit to better absorb volatility.

Spreads are no longer at stressed levels but still reflect some caution on growth. Investment-grade credit is generally seen as resilient due to solid fundamentals, while high yield remains more sensitive to economic slowdown.

The consensus view is that spreads will likely remain range-bound, with only gradual widening if growth weakens, rather than the sharp repricing seen in 2022. However, this remains the consensus as of today.

Overall, within this sub-asset class, investors are attempting to look beyond market noise and focus on optimal positioning.

Credit spreads and equity positioning often move together, with the former sometimes acting as a leading indicator.

Should investors pay closer attention to credit spreads going forward, rather than reacting to short-term equity market moves?

Chart 2. US 5-year Yield vs US Investment Grade Option Adjusted Spread & S&P 500

Source: Bloomberg, ACG Team analysis

Asset class behaviour in an inflation regime

| Asset class | Performance (2022) | Key driver | War linkage |

|---|---|---|---|

| Energy commodities (oil, gas) | Strong positive | Supply shock | Russia = major exporter → prices surged sharply |

| Broad commodities | Positive | Inflation hedge demand | Food + energy shock |

| Global equities | Negative (esp. EU) | Rising rates, growth fears | Risk-off + tightening |

| Government bonds (nominal) | Large negative | Rising yields | Central banks tightening into inflation |

| Inflation-linked bonds | Negative (but less in some cases) | Real yield shock dominates | Duration + rate shock offset inflation accrual |

| Credit (HY/IG) | Negative | Spread widening | Growth + liquidity concerns |

| Gold | Flat to mildly positive | Safe haven | War uncertainty + USD offset |

| USD | Strong | Safe haven + rates | Tightening + risk-off |

| Real estate (REITs) | Negative | Rising discount rates | Rate shock dominates inflation linkage |

| Infrastructure | Relatively resilient | Inflation pass-through | Regulated cashflows |

Source: ECB, BIS, OECD

Euro area inflation rose from around 2.6% to 8.4%, with approximately two-thirds of global economies experiencing inflation levels above 5% (Source: Bank for International Settlements).

Inflation-linked bonds relatively outperformed nominal bonds, with short-maturity issues (0–3y) closing 2022 in the range of 0% to +3%, while nominal bonds ended between -2% and -5%.

For mid- to longer-term maturities, the relative performance gap was less pronounced but still meaningful.

Conclusion: Asset allocation in a regime shift

At ACG, we are currently focused on building portfolios that can navigate geopolitical tensions without distorting investors’ risk-reward profiles and allocations.

To achieve this, both listed and non-listed instruments can play a key role.

Some instruments come with a cost (similar to insurance), while others function as overlays, allowing investors to gain exposure efficiently, including through the use of margin.

More than ever, consistent returns are not achieved by increasing portfolio turnover, but by selecting and applying the right instruments in the appropriate way.

Disclaimer

This newsletter is provided for informational and marketing purposes only and does not constitute investment advice, investment research, or an offer or solicitation to engage in any investment activity.

Past performance is not indicative of future results.

See full legal disclaimer.

For a more detailed discussion on how investors may position portfolios in light of the dynamics described above, please feel free to contact the ACG Team at: acg.group@acg.group

Prepared by

ACG Team